1031 Exchange for Vacant Land in Oregon: Rules, Timelines, and Strategy

________________________________________

1031 Exchange for Vacant Land in Oregon: Rules, Timelines, and Strategy

Yes, you can use a 1031 exchange for vacant land in Oregon — if the land is held for investment purposes and the exchange follows strict IRS guidelines.

A properly structured 1031 exchange allows landowners to:

• Sell investment land

• Defer capital gains taxes

• Reinvest into other real estate

• Potentially move from non-income-producing land into income-producing property

However, the rules are strict, timelines are short, and mistakes can disqualify the exchange.

This guide explains how 1031 exchanges work for vacant land in Oregon, what qualifies, and how landowners can use the strategy effectively.

________________________________________

What Is a 1031 Exchange?

A 1031 exchange refers to Section 1031 of the Internal Revenue Code.

It allows real estate investors to defer capital gains taxes when selling one investment property and reinvesting the proceeds into another like-kind property.

For landowners, this means vacant land can potentially be exchanged for:

• Rental property

• Commercial real estate

• Agricultural land

• Timberland

• Industrial property

“Like-kind” in real estate is broadly defined. Most real property held for investment qualifies.

________________________________________

Does Vacant Land Qualify for a 1031 Exchange?

Vacant land qualifies if it meets two main requirements:

1. The Land Must Be Held for Investment

Land purchased for resale (flipping) does not qualify.

Land held for:

• Long-term appreciation

• Agricultural lease

• Timber harvest

• Investment purposes

typically qualifies.

2. It Must Be Real Property

Personal property does not qualify. Vacant land does.

Intent matters. If the property was held primarily for investment, it likely qualifies.

________________________________________

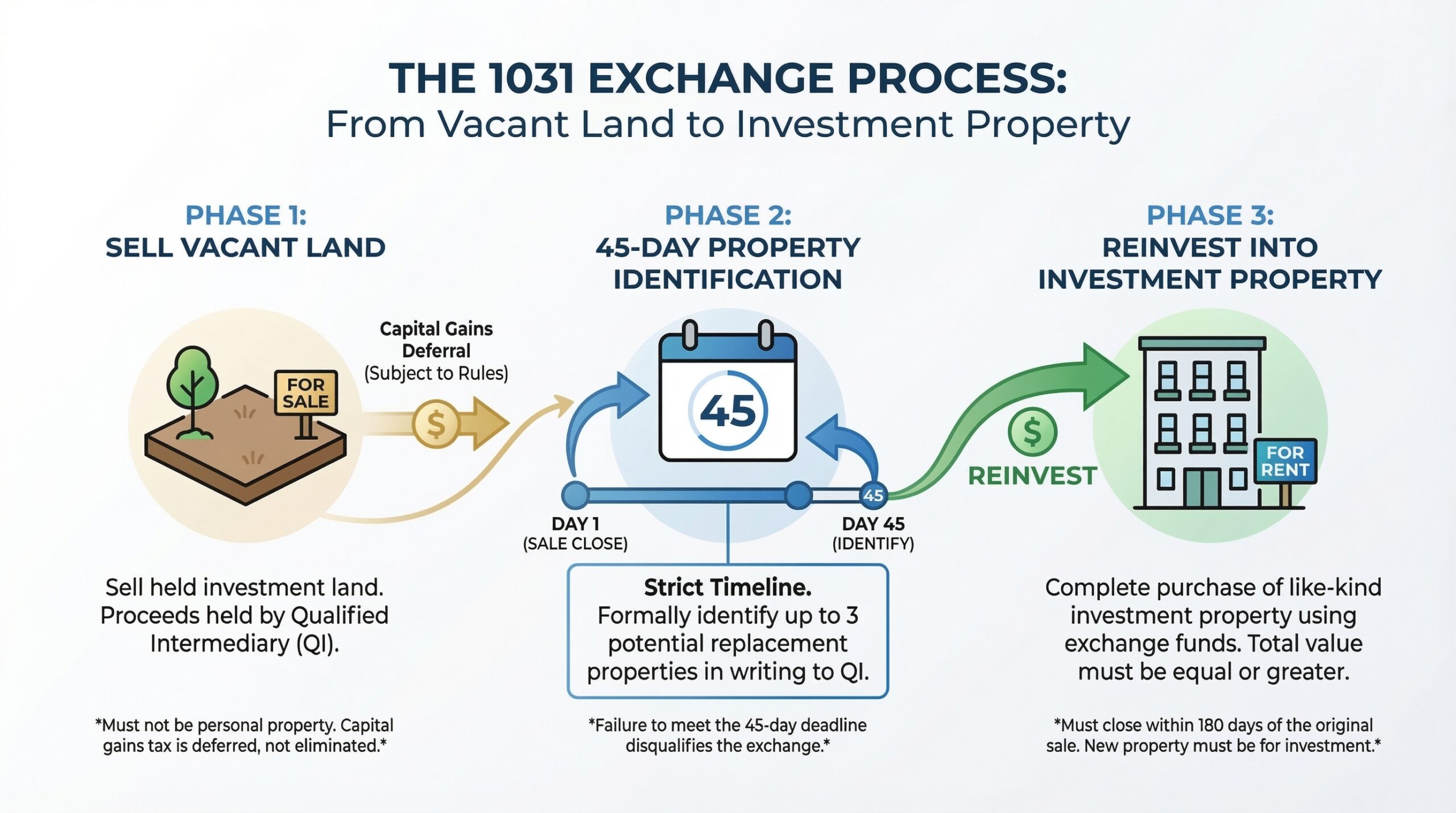

The Two Critical Deadlines

A 1031 exchange is timeline-driven.

There are two strict deadlines:

45-Day Identification Period

Within 45 days of selling your land, you must identify potential replacement property in writing.

You may identify:

• Up to 3 properties (most common method), or

• More under specific value rules

If you miss the 45-day window, the exchange fails.

________________________________________

180-Day Closing Period

You must close on the replacement property within 180 days of the sale of the original land.

This includes the 45-day identification window.

The clock starts the day you close on your land sale.

There are no extensions except in rare federally declared disaster situations.

________________________________________

You Cannot Touch the Money

One of the most common mistakes is taking possession of the sale proceeds.

To qualify for a 1031 exchange:

• Funds must be held by a Qualified Intermediary (QI)

• You cannot receive or control the proceeds

• The QI facilitates the transaction

If you receive the funds directly, the transaction becomes taxable.

Proper structuring before closing is essential.

________________________________________

Why Landowners Use 1031 Exchanges

Many vacant land owners in Oregon hold property that produces no income.

A 1031 exchange allows them to:

• Sell underperforming land

• Defer capital gains taxes

• Reposition into income-producing property

This shifts the investment from appreciation-only to cash-flow-generating.

Income changes the financial profile dramatically.

________________________________________

Example Scenario

A landowner sells vacant land in Oregon for $400,000.

Instead of paying capital gains tax, they:

• Engage a Qualified Intermediary

• Identify replacement rental property

• Reinvest the full proceeds

They purchase a rental generating monthly income.

Now the asset produces:

• Cash flow

• Potential rent growth

• Continued appreciation

The capital gains tax is deferred — not eliminated — but reinvested capital continues working.

________________________________________

What Counts as Like-Kind Property?

In real estate, “like-kind” is broad.

Vacant land can be exchanged for:

• Residential rental property

• Commercial buildings

• Agricultural land

• Timberland

• Industrial property

Primary residences do not qualify.

The replacement property must also be held for investment.

________________________________________

Oregon-Specific Considerations

In Oregon, landowners should consider:

• Zoning classification

• Agricultural or forest deferral status

• Development limitations

• Timber value

• Urban growth boundary placement

Before initiating an exchange, evaluate whether the land is:

• Truly investment property

• Eligible under current use classification

Consultation with tax professionals is important when special land classifications apply.

________________________________________

Common Mistakes to Avoid

1. Waiting Too Long to Plan

You must structure the exchange before closing the sale.

2. Missing the 45-Day Identification Deadline

The timeline is strict.

3. Improper Property Identification

Identification must be written and precise.

4. Taking Control of Funds

You cannot touch the sale proceeds.

5. Buying Property for Personal Use

Replacement property must be investment property.

Mistakes can result in full capital gains taxation.

________________________________________

When a 1031 Exchange Makes Strategic Sense

A 1031 exchange is often beneficial when:

• Vacant land produces no income

• Appreciation has plateaued

• Capital gains tax exposure is significant

• Replacement property offers income

• Long-term repositioning is desired

It is less beneficial when:

• Land has near-term development potential

• The owner plans to exit real estate entirely

• Replacement property cannot be identified within timeline

Strategy matters more than tax deferral alone.

________________________________________

Deferral vs Elimination

A 1031 exchange defers capital gains tax — it does not eliminate it.

Taxes may eventually be due if:

• Replacement property is sold without another exchange

• Investment intent changes

However, continued exchanges may defer taxes long-term.

Estate planning strategies can also influence tax outcomes.

Professional tax advice is essential.

________________________________________

Is a 1031 Exchange Always the Best Move?

Not necessarily.

Factors to evaluate include:

• Replacement property quality

• Income potential

• Market timing

• Personal financial goals

• Long-term strategy

A poor replacement property can create greater risk than holding land.

The exchange must align with financial objectives.

________________________________________

Frequently Asked Questions

Can you use a 1031 exchange on vacant land in Oregon?

Yes, if the land was held for investment and exchange rules are followed.

Does the replacement property have to be land?

No. It can be most types of real estate held for investment.

What happens if I miss the 45-day deadline?

The exchange fails, and capital gains taxes apply.

Can I live in the replacement property?

Not immediately. It must be held for investment purposes.

Do I need a professional intermediary?

Yes. A Qualified Intermediary is required.

________________________________________

Final Analysis

A 1031 exchange can be a powerful strategy for Oregon landowners holding vacant property.

It allows deferral of capital gains taxes and repositioning into income-producing assets.

However, strict timelines and procedural rules apply.

The strategy works best when:

• Land no longer fits long-term goals

• Income is desired

• Capital can be redeployed more productively

A 1031 exchange is not just a tax tool — it is a portfolio restructuring tool.

When used strategically, it can shift an asset from speculation to structured growth.

Bare Land vs Rental Property in Oregon: Which Builds Wealth?